Background

The utilization of automatic features in defined contribution plans has increased significantly since they were first introduced as part of the Pension Protection Act of 2006 (PPA). More plans are adopting these provisions, resulting in higher participation rates among employees. Although this is a positive trend, certain design features actually thwart the success that could otherwise be achieved. Specifically:- relatively low default deferral rates result in lower savings;

- automatic enrollment is often applied to newly eligible employees only, disregarding existing employees who are not participating; and

- auto-escalate provisions, if used, are often applied on an opt-in basis rather than an opt-out basis, and at rates too low to achieve targeted savings levels.

Default Deferral Rates

A recent study by Aon Consulting found that participants should save 15% of their pay, including employer contributions, over their working career to provide adequate retirement income. To the extent employees wait to enroll in the plan or enroll at lower contribution levels, the required contribution amount increases.Multiple studies consistently show that the majority of plans using automatic enrollment use a default rate of 3% savings. This rate mirrors the safe-harbor guidelines, but is required to be used only if adopting a safe-harbor plan, which most plans are not. The 3% rate also is generally believed to be the rate likely to reduce the level at which participants opt out of the program, although there is no empirical evidence suggesting this is the case. Several studies suggest default contribution rates could be increased significantly without a meaningful increase in opt-outs.

To improve the overall savings rates of participants, plan sponsors should auto-enroll all eligible employees at a higher initial default rate. If practical, the initial default contribution rate should be tied to the plan’s maximum matching contribution percentage.

Automatic Enrollment

While automatic enrollment has increased in popularity, the majority of plans only use it to enroll newly eligible employees, perhaps missing other opportunities. At a minimum, plan sponsors should apply auto-enroll to all employees at the time of adoption of the auto-enroll feature. To enhance the program further, a periodic reenrollment of all non-participating employees should be conducted. This can often coincide with the open enrollment period for other employee benefits.Automatic Contribution Escalation

Automatic contribution escalation, used in conjunction with auto-enrollment, offers a powerful opportunity to improve participant outcomes. To maximize its impact, auto-escalate should be offered on an opt-out basis rather than an opt-in basis. A recent study has shown that of those plans offering auto-increase on an opt-out basis, nearly 65% of participants remained in the program. Where auto-increase was made available on an opt-in basis, only 8% of participants chose to opt in.Auto-escalate can be enhanced even further by increasing the contribution rate by more than 1% per year. Assuming an initial deferral rate of 3% with 1% annual increases, it will take more than seven years to achieve a double-digit savings rate. An initial rate of 6% combined with 2% annual increases will achieve this level in three years.

Improved Participant Outcomes

By combining auto-enrollment with auto-escalate and increasing the initial default deferral rate, participants can significantly increase their savings over time. Just as participant inertia keeps employees from enrolling in the plan, so, too, can it put them on the path to a more secure retirement when effective auto-features are implemented.

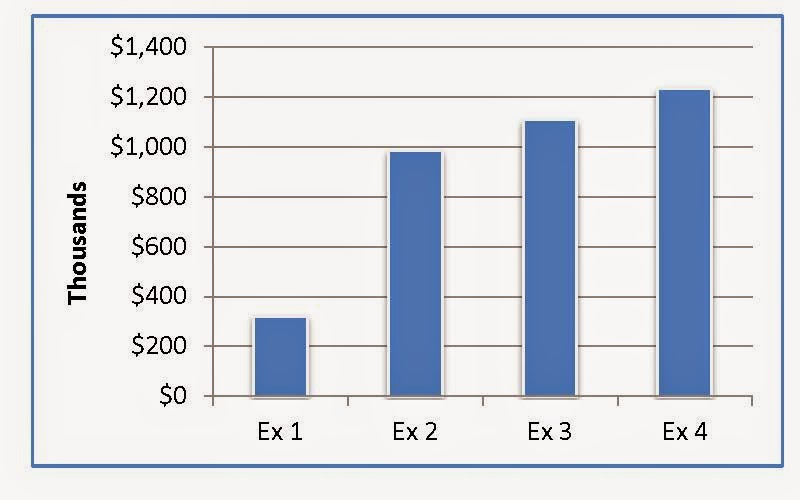

The chart shows projected participant account balances for four different scenarios[1]. Example 1 assumes a default rate of 3% with no auto-escalate provision; Example 2 implements auto-escalate at 1% while Example 3 implements auto-escalate at 2%. Finally, Example 4 sets the default rate at 6% combined with an auto-escalate rate of 2%.

The chart shows projected participant account balances for four different scenarios[1]. Example 1 assumes a default rate of 3% with no auto-escalate provision; Example 2 implements auto-escalate at 1% while Example 3 implements auto-escalate at 2%. Finally, Example 4 sets the default rate at 6% combined with an auto-escalate rate of 2%.Conclusion

Employers are faced with a number of challenges in designing and offering an effective and meaningful retirement program, particularly in light of budget limitations. By designing a program that uses comprehensive automatic features, participant outcomes can be significantly improved within fiscal constraints.This article addresses some steps plan sponsors can take to improve participation rates and overall savings rates within defined contribution retirement plans. To read about other plan design changes that can improve participant readiness, read Improving Participant Outcomes: An Action Plan for Plan Sponsors.

If you have any questions about this article, or would like to begin talking to a dedicated retirement plan advisor, please get in touch by email or by calling (855) 882-9177.

* * *

[1] All examples assume an initial salary of $45,000 with 3% annual increases. Employee contributions are capped at 15% with an employer match of 50% up to 6% of salary. Account balances are projected over 30 years at an assumed rate of 8%.